Applied Materials: A Decade of Market Share Stagnation Under Dickerson’s Leadership

I have been critical of Applied Materials (AMAT) ever since Dickerson and his team took over following the 2011 acquisition of Varian Semiconductor Equipment Associates (VSEA). Through my analysis, I have consistently highlighted the company's declining market share, not just against key competitors but across the broader WFE market. Despite clear empirical data supporting this trend, sell-side analysts continue to push a bullish narrative on the stock. This article serves as yet another effort to inform investors that the tactics AMAT employs to influence these analysts into issuing Buy ratings fail to align with the actual market reality.

Chart 1 shows AMAT’s share of the WFE market since 2011, and the trendline (dotted) shows the change in global market share, which is flat through 2024. This despite the fact that in 2019 AMAT management took $331 million from 2018 revenues and put them in 2019 in response to concern that ASML (ASML) might take over the global #1 position as semiconductor equipment supplier. In fact, for the first time in 20 years, ASML did indeed dethrone AMAT, and it did it again in 2023 and 2024, according to my report at The Information Network entitled Global Semiconductor Equipment: Markets, Market Shares and Market Forecasts

Chart 1

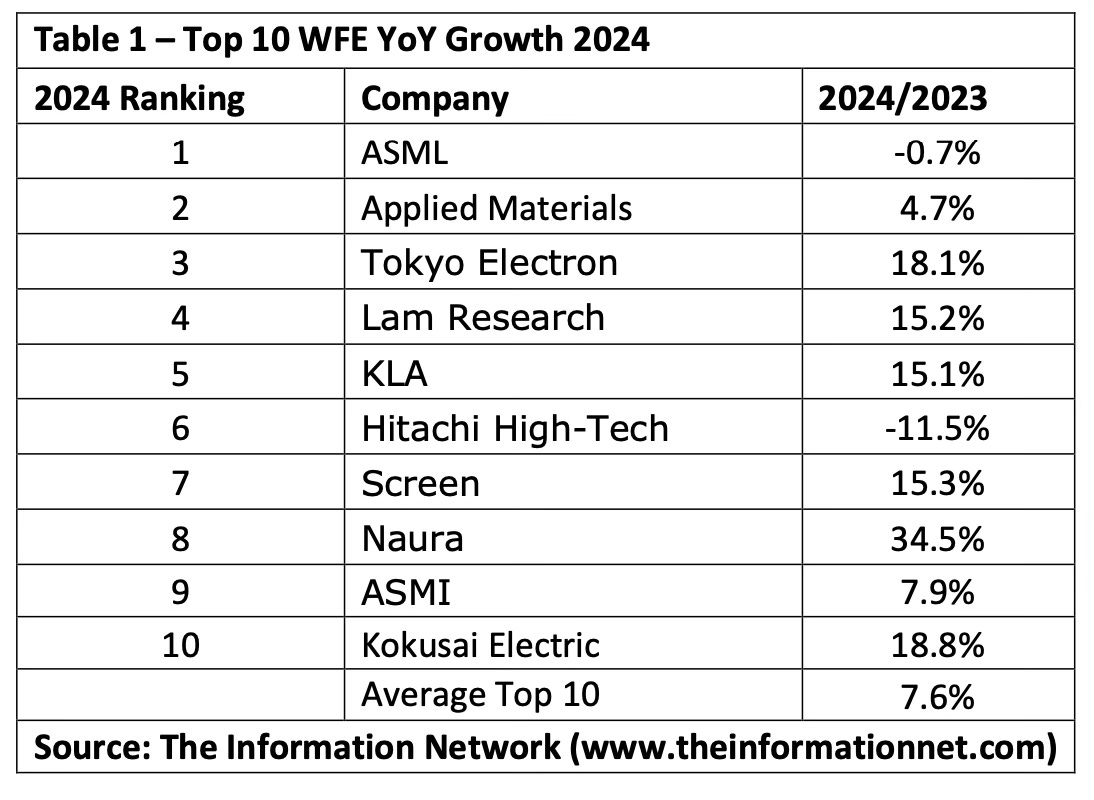

Table 1 shows revenue for the Top 10 WFE equipment companies for 2024. AMAT’ YoY revenue grew 4.7% compared to an average of 7.6% for the Top10 (including AMAT), showing AMAT lost market share to top WFE companies and leading competitors such as Lam Research (LRCX), Tokyo Electron (TOELY), Kokusai Electric (KOKSF), ASM International (ASMIY) and China’s Naura in etch and deposition, and KLA (KLAC) in metrology/inspection.

Why is this important. With AMAT as the top #1 or #2 company, it should have the resources to hire the best employees and spend the most R&D money to make the most sought-after state-of-the-art equipment. Evidently it does not.

Secondly, when a company loses market share to a competitor, it means it didn’t have the “best-of-breed” equipment to win the sale. Not only that, but when the customer decides to acquire more of the same in a “capacity purchase” it will again buy more from the competitor.

This lack of share growth rests solely on the CEO Gary Dickerson.

AMAT’s Recent Earnings Call

AMAT announced its fiscal Q1 2025 earnings call on February 13. Other investors didn’t like the results either, as the stock dropped 8.2% the next day.

My negative view on Applied Materials is well-supported by the company’s own statements on the call. Key concerns, which I will detail in this article, include:

1. Geopolitical Headwinds – $400M revenue loss in FY2025 from China restrictions, and further market share loss to domestic Chinese competitors.

2. ICAPS Slowdown – After strong spending in 2023-24, ICAPS demand is softening, creating near-term headwinds

3. DRAM Equipment Demand is Weak – Despite AI-driven HBM demand, DRAM equipment orders remain sluggish.

4. Packaging Growth May Not Be Enough – While expanding, packaging remains a small portion of overall WFE revenue.

5. Uncertain Market Share Gains – Applied is dependent on foundry investments in new nodes, which may not materialize at expected rates.

6. Reliance on Buybacks – Record EPS was fueled by share repurchases rather than business growth.