Arm Thinks AI Agents Will Trigger A CPU Supercycle

What’s in This Article

Introduction

Chart 1: Arm’s AI Total Addressable Market Forecast FY2026–FY2031

Table 1: Arm AI Market Opportunity By Application

Arm’s Record Quarter Masks A Strategic Shift

Table 2: Arm FY2026 Financial Performance

The AGI CPU Changes Arm’s Business Model

Table 3: Hyperscaler Adoption Of Arm-Based AI CPUs

Why AI Agents Increase CPU Demand

Table 4: CPU Core Scaling Versus GPU Scaling

Supply Constraints And The New CPU Arms Race

Investor Takeaway

Introduction

Arm Holdings plc (ARM) has spent decades building the architectural foundation underneath the global smartphone industry. Founded in 1990 as a joint venture between Acorn Computers, Apple (AAPL), and VLSI Technology, Arm operated as a semiconductor intellectual-property company that licensed CPU architectures and core designs to semiconductor companies rather than manufacturing chips itself. Over the next three decades, Arm evolved into the dominant CPU architecture supplier for smartphones and embedded devices, with its designs incorporated into billions of chips annually across mobile, networking, automotive, and cloud infrastructure markets.

In September 2020, Nvidia (NVDA) attempted to acquire Arm from SoftBank for approximately $40 billion in order to strengthen its position in AI and edge computing, but the transaction collapsed in February 2022 following regulatory opposition in the United States, Europe, and China. SoftBank instead completed Arm’s Nasdaq IPO in September 2023 at $51 per share, with strategic investors including Apple, Nvidia, AMD (AMD), Intel (INTC), Alphabet (GOOGL), Samsung, and Taiwan Semiconductor Manufacturing (TSM) participating in the offering.

For years, investors viewed artificial intelligence primarily through the lens of GPUs and accelerators. Nvidia’s dominance in AI training reinforced the idea that CPUs would gradually become less important as accelerators absorbed larger portions of AI workloads. Arm’s recent earnings call challenged that assumption directly.

CEO Rene Haas argued repeatedly that AI agents and heterogeneous computing systems increase CPU importance rather than diminish it. According to management, CPUs are becoming critical orchestration engines responsible for task scheduling, memory management, networking, security, and coordination among accelerators. As AI systems become increasingly agentic and autonomous, CPU demand may expand dramatically alongside GPUs rather than being displaced by them.

This thesis arrives as Arm itself undergoes a strategic transformation. Historically, the company generated revenue primarily through licensing its architecture and collecting royalties on chip shipments. That business model began changing in 2025 with the introduction of Arm’s AGI CPU program, under which the company started offering direct CPU products targeting hyperscale AI infrastructure.

Arm’s AI Total Addressable Market Forecast FY2026–FY2031

According to Chart 1, Arm estimates its total AI-related addressable market will expand from approximately $535 billion in FY2026 to more than $1.5 trillion by FY2031. The largest growth category is Cloud AI, where XPU opportunity alone is projected to exceed $1 trillion by FY2031.

The chart also highlights that Arm’s AI strategy now spans three major segments: Cloud AI, Edge AI, and Physical AI. While Edge AI remains a substantial opportunity, Cloud AI infrastructure increasingly represents the company’s most important long-term growth driver.

Most importantly, Arm projects the AI data-center CPU opportunity to expand from approximately $50 billion to more than $100 billion by FY2031. This forecast directly supports management’s argument that CPUs remain central to AI infrastructure despite the rapid expansion of accelerators and GPUs.

Chart 1 – Arm AI TAM Forecast FY2026–FY2031

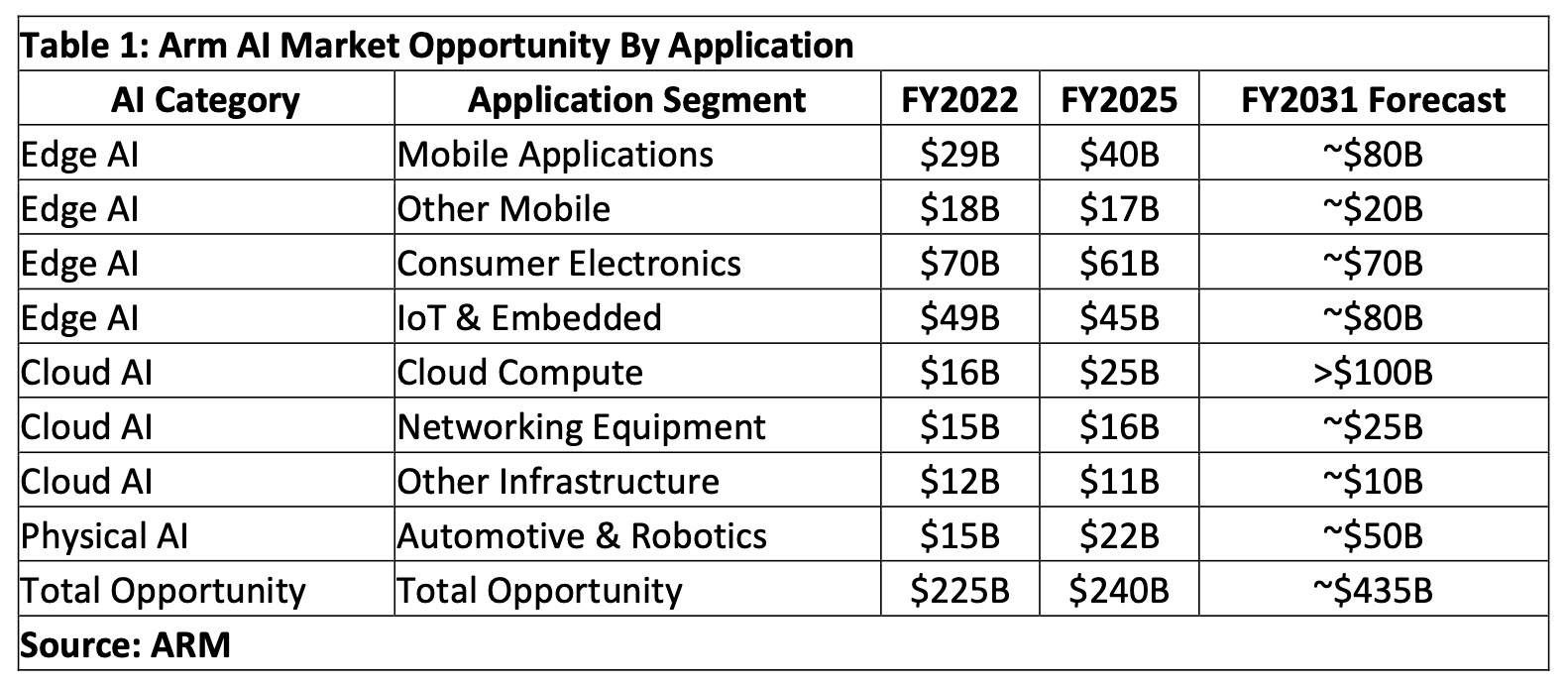

Arm AI Market Opportunity By Application

According to Table 1, Arm’s long-term AI opportunity spans far beyond smartphones and PCs. Within Edge AI, the company projects substantial growth in mobile applications and IoT and embedded systems, each approaching approximately $80 billion by FY2031. In Cloud AI, the largest opportunity comes from cloud compute, which Arm estimates will expand from approximately $25 billion in FY2025 to more than $100 billion by FY2031 as hyperscalers increasingly adopt Arm-based CPUs for orchestration and AI infrastructure. Meanwhile, Physical AI represented primarily by automotive and robotics applications is projected to more than double from $22 billion to approximately $50 billion over the same period.