Flat Semiconductor Shipments Reshape the Industry: Winners and Losers in the High-ASP Era

Before I begin, in 2025 The Information Network celebrates its 40 year anniversary. I notified Paid Subscribers yesterday that many of the reports I publish are offered at 1985 prices of $995 (vs $4,995 today). But its only for Paid Subscribers. Sign up now as a Paid Subscriber and take advantage of this Once in a Lifetime Offer, which ends March 31. Contact me for details.

This past week I spoke at Bank of America’s 2025 Asia Tech Conference in Taiwan on March 17-21, 2025. https://gems.bankofamerica.com/public/EventOverview.do?dispatch=display&eventId=iCCvaYtykzY=&inviteeId=&authKey=bAf/ysNoQdEtk8wyaVWMhVOjT1fS55bUTTdvsRQilqW/ENIERgwrvdjslW/5xSaQiVdZrIhSUNM=&site=client&isFromTestAndView=Y#/overview

The title of my presentation was “AI Semiconductor Market: Driving Computing, AI, and Industry Innovation” and this article expands the part of my presentation on the AI Semiconductor Market Cycle.

Semiconductor Units vs. Revenue Growth: A Deep-Dive Analysis

The semiconductor industry is undergoing a fundamental transformation, where revenue growth is decoupling from unit shipment expansion. Traditionally, revenue growth was strongly correlated with the number of chips produced, as higher unit shipments drove top-line increases. However, in 2024, this relationship has weakened significantly due to a shift in value from volume-driven sales to pricing power enabled by advanced technology.

Breaking Down the Numbers: The Unit-Revenue Gap

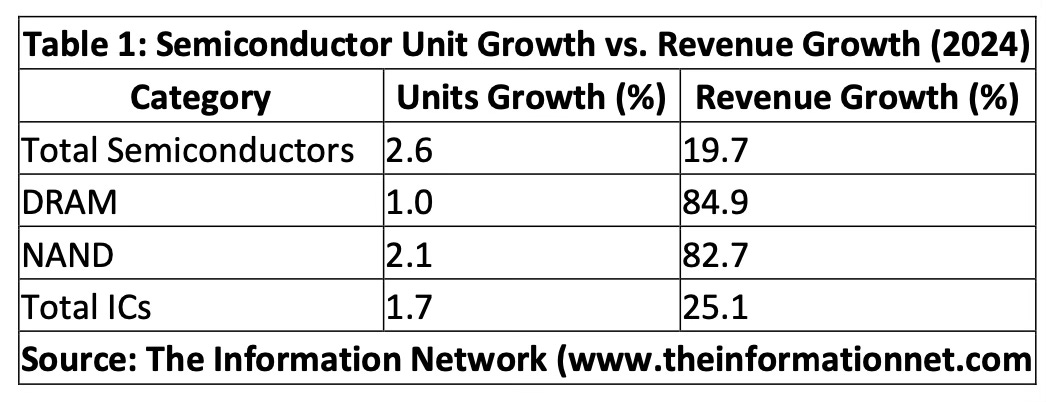

At first glance, the modest increase in semiconductor unit shipments—just 2.86% overall—suggests a relatively stagnant market. However, revenue has jumped by 19.7%, highlighting the growing impact of rising average selling prices (ASPs) and a shift toward more technologically advanced chips. The most extreme case is in DRAM, where revenue surged by 84.9% despite unit shipments rising just 1.0%. This trend is also visible in NAND flash, with an 82.7% revenue increase versus just a 1.7% growth in shipments.

Table 1 highlights how revenue growth has far outpaced unit growth across all major semiconductor categories, underscoring the increasing role of ASPs in driving revenue, according to my report at The Information Network entitled Global Semiconductor Equipment: Markets, Market Shares and Market Forecasts.

A key reason for this disconnect is the rising average selling prices of semiconductor components. This trend has been particularly strong in memory and high-performance logic chips, where demand is concentrated in advanced process nodes that require higher manufacturing costs. With each new technology node, the cost per wafer and per transistor rises, leading to higher ASPs even when unit shipments remain flat.

Chart 1 illustrates semiconductor Unit Growth from July 2019-December 2024.

Chart 1

While Chart 2 shows Semiconductor Revenue for the same period.