Foundry Power in 2030: Why China Will Lead in Capacity but Taiwan Will Still Rule the Market

Introduction

The great paradox of the semiconductor century is now before us: China is surging to the top in terms of pure manufacturing capacity, yet Taiwan is positioned to maintain its unassailable leadership in revenue. This dichotomy reflects the central law of silicon economics: not all wafers are created equal. In the foundry arena, sheer volume no longer defines supremacy—value per wafer, node leadership, and ecosystem lock-in are now the currency of power.

By 2030, China is expected to operate more foundry capacity than any other country. This milestone, once unthinkable in a domain long dominated by Taiwan, Korea, and the U.S., reflects years of aggressive investment by firms like SMIC, Hua Hong, Nexchip, and others. Yet even as China's 8-inch equivalent wafer output races toward 2 million wafers per month, most of those wafers will be etched with nodes far coarser than those emerging from Taiwan’s 2nm fabs. The divide between capacity and capability has never been starker.

Investors, analysts, and policymakers now face a bifurcated map of global silicon power. On one axis lies total volume—measured in kilowafers per month—on the other, strategic value, dictated by the number of transistors per square millimeter and the scarcity of high-end packaging infrastructure. The tables that follow—corrected and updated to reflect 2025–2030 trajectories—reveal that although China may top the volume charts by the end of the decade, Taiwan will still command the value stack. The difference between running fabs and leading nodes will define the competitive arc of the next era in semiconductors.

The 2025 Landscape: Volume Favors China, Value Favors Taiwan

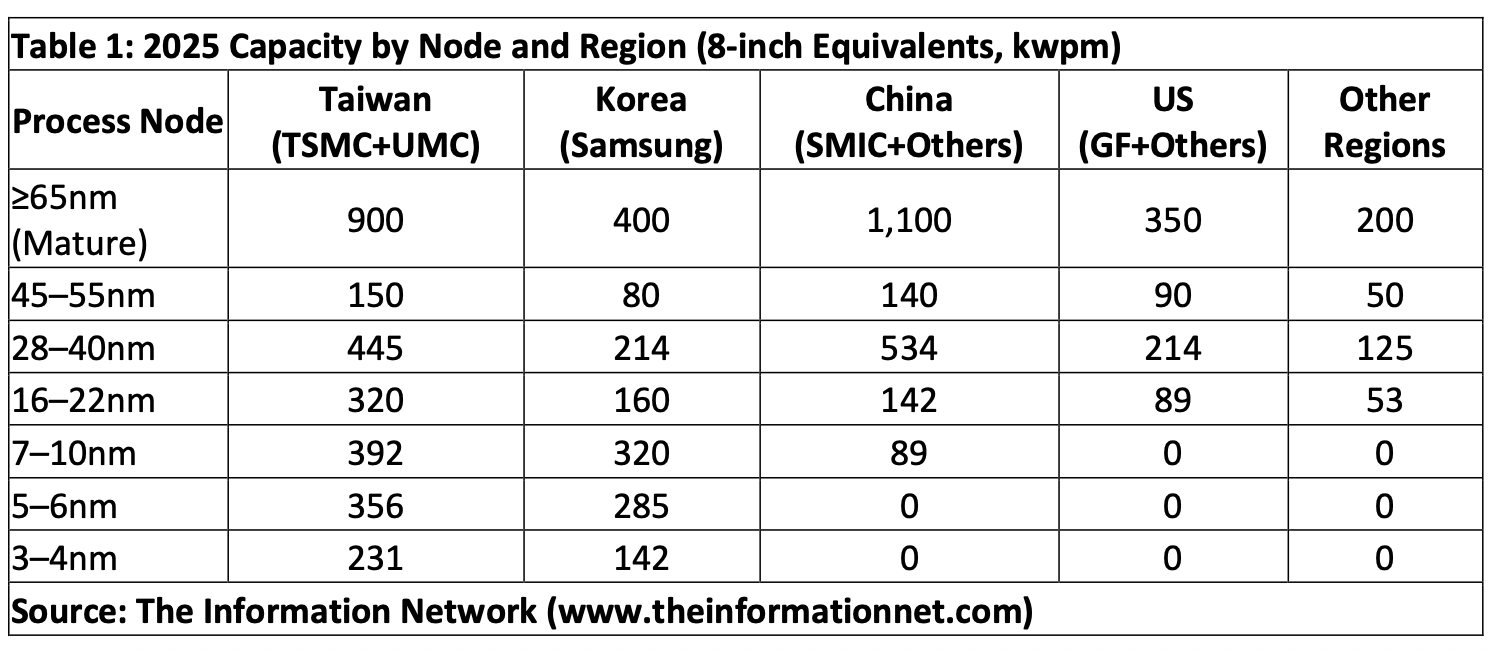

According to Table 1, the global semiconductor foundry landscape in 2025 is bifurcated by design and destiny. On one side sits the volume buildout — a mass of capacity in mature nodes like 65nm and 45nm, driven by auto ICs, power management chips, and microcontrollers. On the other sits the value front, advanced logic nodes at 5nm and below where margins soar and complexity concentrates. When measured in 8-inch equivalents, China has already taken the lead in physical volume at mature nodes, with 1,100 kwpm of ≥65nm capacity — far outpacing Taiwan, Korea, or the U.S. Taiwan, by contrast, leads in advanced-node throughput, with nearly 600 kwpm at ≤10nm alone, according to The Information Network report entitled “Global Semiconductor Equipment: Markets, Market Shares and Market Forecasts.”

The regional divergence is more than technical — it is geopolitical. Taiwan and Korea continue to invest in high-value node transitions, while China adds capacity at legacy nodes as a hedge against export control regimes and to support domestic substitution. The U.S. remains modest in volume but increasingly strategic in node targeting through the CHIPS Act and Intel’s resurgence.