Nvidia, TSMC and ASML – Three Companies That Won’t Have Significant Competition For the Next 5 Years

In the competitive landscape of the semiconductor industry, conducting thorough company analysis is essential for investors and industry experts. This article will provide an in-depth industry comparison, focusing on NVIDIA, TSMC, and ASML alongside their major competitors. By examining key financial metrics, market positions, and growth potential, we aim to deliver valuable insights for investors and offer a deeper understanding of each company's performance within the industry.

Nvidia and Competition

Nvidia is a prominent developer of graphics processing units (GPUs). Initially, GPUs were primarily used to improve computing experiences, particularly in gaming on PCs. However, their applications have broadened significantly, making them crucial components in artificial intelligence (AI). Nvidia provides not only AI-focused GPUs but also a software platform called CUDA, which is essential for AI model development and training. Additionally, Nvidia is expanding its data center networking solutions to integrate GPUs for managing complex workloads.

Chart 1 shows the dominance of Nvidia at the data center through Q1 2024 compared to that off data center processor competitors AMD and Intel.

Currently, it seems improbable that any new companies will emerge as major players in the GPU market alongside Nvidia. Even Intel, a giant in the chip industry, has struggled to produce a high-end GPU that appeals to gaming enthusiasts, with its next attempt at a discrete GPU slated for 2025. This highlights Nvidia’s dominance in the GPU market, with minimal competition expected in the near future.

GPUs are well-suited for handling the extensive calculations required by Large Language Models (LLMs) like GPT-3, which involves training on a massive number of parameters—175 billion in the case of GPT-3. Nvidia has strategically secured its dominance in this area through the development and expansion of the CUDA software platform. CUDA offers a comprehensive suite of proprietary libraries, compilers, frameworks, and development tools that AI professionals rely on to build their models. Importantly, CUDA is exclusive to Nvidia GPUs, creating significant switching costs for customers and reinforcing Nvidia's competitive edge.

Even if a competitor could develop a GPU comparable to Nvidia's, the code and models built on CUDA may not easily transfer to a different GPU. This gives Nvidia a substantial advantage. As a result, any company involved in LLM development risks falling behind while awaiting alternatives, as Nvidia continues to lead the field.

TSMC and Competition

The semiconductor foundry market is undergoing significant changes as leading players TSMC, Samsung, and Intel ramp up their competition to dominate advanced manufacturing processes. Each company brings unique strengths and strategies, shaping the industry's future over the next five years.

Current Market Position and Technological Leadership

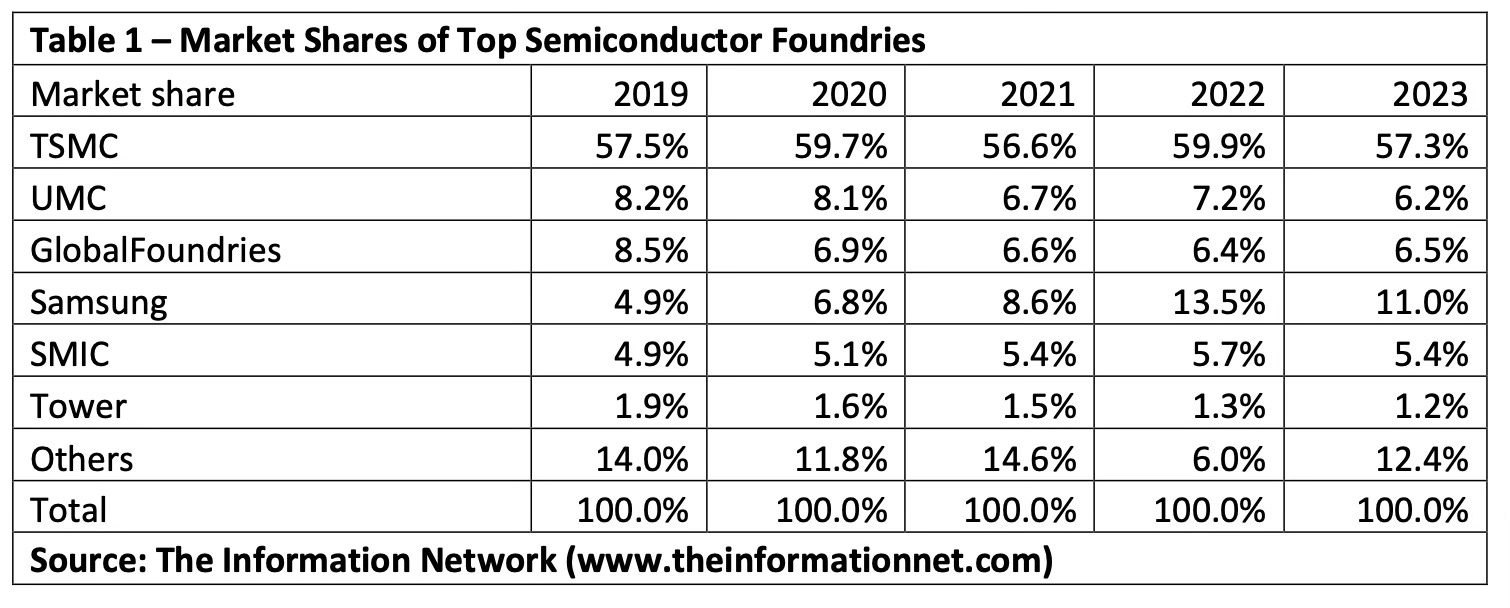

TSMC is the undisputed leader in the semiconductor foundry market, holding a 57% of the global market share as of 2023 (Table 1). It has established itself as the preferred foundry for high-performance computing and mobile devices, with its 5nm and 3nm nodes setting industry standards. The company is also pushing for 2nm production by 2025, further cementing its technological leadership, according to The Information Network’s report entitled Global Semiconductor Equipment: Markets, Market Shares and Market Forecasts.

Samsung Foundry, with around 11% market share, is TSMC's closest rival. Samsung has made significant strides in advanced node technology, starting mass production of its 3nm Gate-All-Around (GAA) process in 2022. This technology promises improvements in power efficiency and performance, positioning Samsung as a formidable competitor. The company plans to start 2nm production by 2025, directly challenging TSMC's timeline.

Intel Foundry Services (IFS), a newer player in the foundry market, is leveraging its extensive semiconductor manufacturing experience to carve out a niche. Historically focused on its processors, Intel is now expanding its foundry services to external customers. Its IDM 2.0 strategy, announced in 2021, includes significant investments in new fabs and advanced nodes like Intel 20A (equivalent to 2nm) and Intel 18A, with production slated for 2024 and 2025, respectively.

Key Areas of Competition

Advanced Manufacturing Processes:

TSMC: