Riding the Solar Wave: Investing in China's Dominance of the Global Photovoltaic Industry

Summary

China leads the global PV market, dominating manufacturing across the value chain but facing geopolitical and trade risks.

Advanced technologies like HJT and TOPCon drive efficiency, with leaders like JinkoSolar and LONGi Green at the forefront.

Potential Trump 2.0 sanctions could disrupt Chinese manufacturers, while non-Chinese players like First Solar (+28.21% YTD) thrive.

Oversupply and price declines in polysilicon and modules weigh on Chinese firms like Daqo (-17.50%) and JinkoSolar (-31.55%).

Diversification is key, with non-Chinese resilience complementing potential recovery in undervalued Chinese stocks.

Global Photovoltaic Industry

The global photovoltaic industry is undergoing a transformative period, with China's dominance presenting unparalleled investment opportunities, according to The Information Network’s report entitled Opportunities in the Solar Market for Crystalline and Thin Film Solar Cells.

As advanced technologies revolutionize solar energy, the question isn't whether to invest in this burgeoning sector but how to position your portfolio for maximum gains.

The global photovoltaic industry has witnessed unprecedented growth over the past two decades, with China emerging as the undisputed leader across nearly every segment, from silicon materials to solar modules. This dominance is no accident. It is the result of massive government support, an expansive manufacturing ecosystem, and consistent technological innovation. For investors, China’s solar supremacy presents a compelling opportunity to tap into the renewable energy revolution.

Companies to Watch

China’s solar dominance is driven by innovative companies leading the global photovoltaic value chain. Investors can capitalize on this growth by focusing on these key players:

JinkoSolar (Ticker: JKS): A global leader in solar cells and modules, driving efficiency with advanced TOPCon technology. Its ADR listing makes it accessible to U.S.-based investors.

Huasun Energy: An emerging powerhouse in heterojunction (HJT) and zero busbar (0BB) technologies, with the potential for international expansion into the U.S. market.

LONGi Green Energy: The undisputed leader in monocrystalline silicon wafers and high-efficiency modules, poised for future U.S. ADR offerings.

First Solar (Ticker: FSLR): A dominant U.S.-based player specializing in CdTe thin-film technology, providing complementary exposure to non-Chinese solar innovation.

These companies represent the best opportunities to ride the solar wave while aligning portfolios with the renewable energy transition.

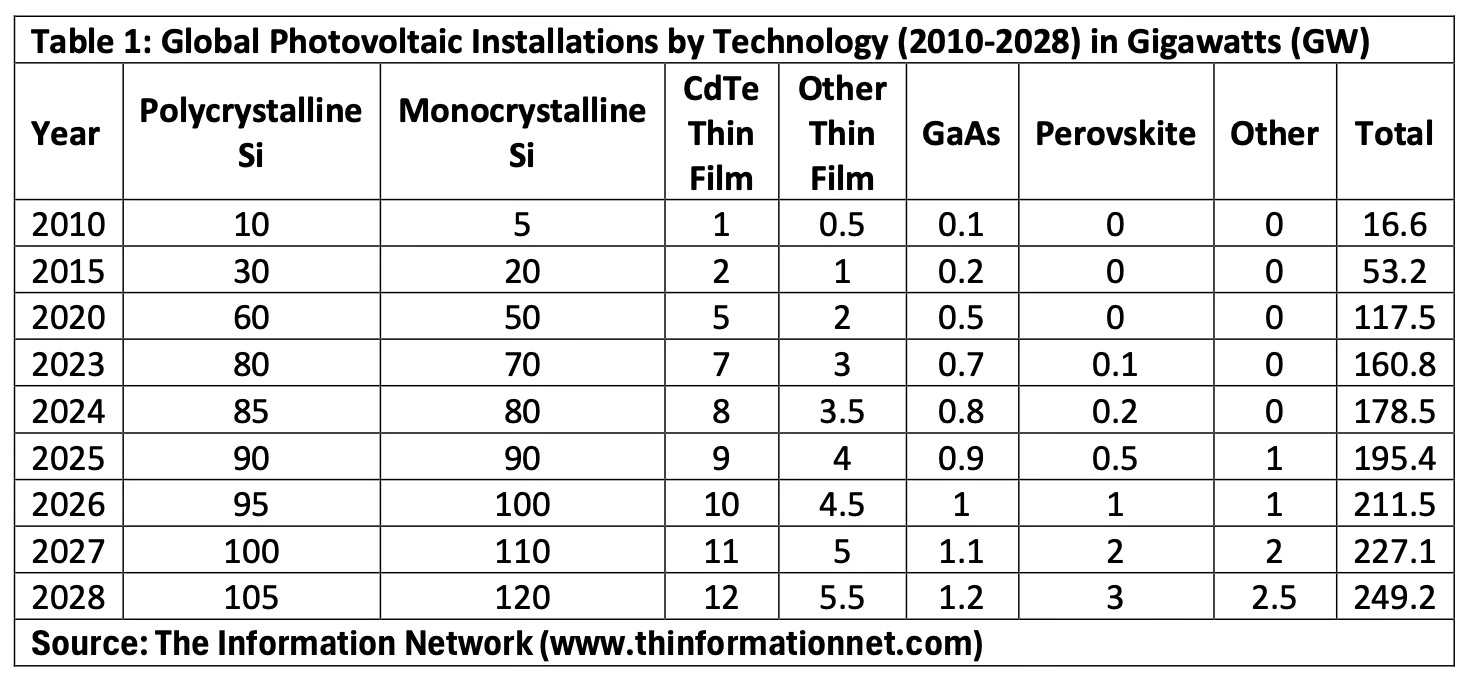

Table 1 represents the segmentation of global PV installations by technology type, including polycrystalline Si, monocrystalline Si, CdTe thin-film, GaAs, perovskite, and others. Over the years, monocrystalline silicon has surpassed polycrystalline silicon as the dominant technology due to its higher efficiency and falling production costs. Thin-film technologies, such as CdTe and GaAs, occupy niche markets with specific applications, including utility-scale installations and space exploration. Emerging technologies like perovskite started gaining traction post-2023 and are projected to grow rapidly due to their potential for high efficiency and low manufacturing costs. The "Other" category includes experimental and hybrid technologies not yet commercially widespread.

Advanced Cell Technologies in Photovoltaics: 2023-2028

The adoption of advanced photovoltaic cell technologies, including xBC, 0BB, HJT, and TOPCon, has revolutionized solar energy by offering higher efficiency and reliability. Due to the many advances in photovoltaic technology over the last decade, the average panel conversion efficiency has increased from 15% to over 23%.

These technologies are reshaping utility-scale and high-performance applications, and their market penetration is projected to grow significantly by 2028. Below is a detailed explanation of each technology, followed by Chart 1 illustrating the differences in technologies.