SemiAnalysis Is Right About Memory. AI Economics Will Decide the Winners

What’s in This Article

Introduction

The Memory Story Is Real

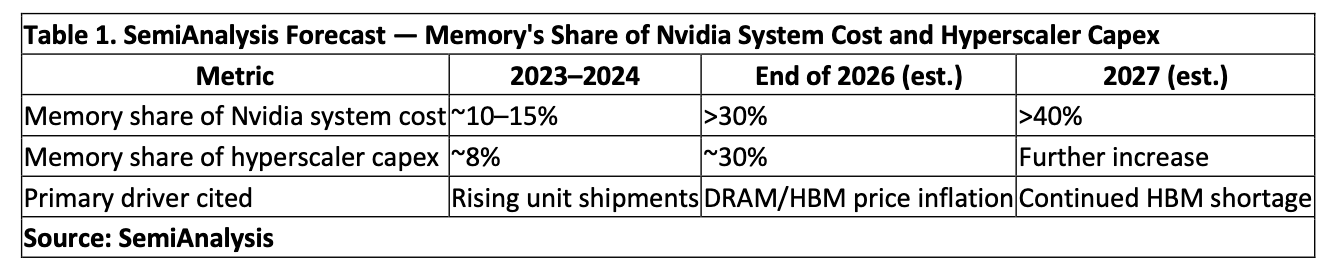

Table 1. SemiAnalysis Forecast — Memory’s Share of Nvidia System Cost and Hyperscaler Capex

Revenue Growth, Not Component Cost, Determines Investment Returns

Table 2. Scenario Inputs and Required Revenue per Productive GPU-Hour

Table 3. AI Infrastructure Economics Framework

Revenue per Rack Remains the Metric That Matters

Table 4. AI Infrastructure Economic Value Chain

Investor Takeaway

Introduction

One of the most widely discussed semiconductor reports this week came from SemiAnalysis, which argued that memory will account for more than 30% of Nvidia AI system spending by the end of 2026 and exceed 40% during 2027. Their conclusion represents an important shift in how investors should think about artificial intelligence infrastructure. For years, GPUs dominated discussions surrounding AI hardware economics. SemiAnalysis correctly argues that memory is no longer a secondary consideration. It has become one of the largest cost elements inside next-generation AI systems.

I believe that conclusion is fundamentally correct. High-bandwidth memory has evolved from a supporting component into a strategic technology that increasingly determines AI system performance, product availability, and capital allocation throughout the semiconductor industry. As Nvidia’s roadmap has accelerated and each successive architecture requires substantially more HBM capacity, memory suppliers have redirected manufacturing toward higher-value AI products, fundamentally changing pricing throughout the broader DRAM market. I recently argued that Nvidia has not merely benefited from the AI memory boom—it has effectively rewritten the economics of the memory industry by influencing where billions of dollars of manufacturing investment are directed.

This is where SemiAnalysis’s contribution to this article ends. The firm’s supply-chain analysis and conclusions regarding rising memory content are well supported. The investment question, however, begins where that analysis ends.

Investors do not earn returns because memory represents 30% rather than 20% of an AI rack. They earn returns because those racks generate sufficient cash flow to recover their capital cost while producing attractive returns on invested capital. Memory pricing affects those economics, but it does not determine them. Cost composition and investment economics are related, yet they answer fundamentally different questions.

This distinction becomes increasingly important as hyperscalers prepare to spend hundreds of billions of dollars expanding AI infrastructure over the next several years. Wall Street has largely debated whether AI capital expenditures remain sustainable. SemiAnalysis adds an important new variable by showing that memory will consume an increasing share of those investments. The more important question for investors, however, is whether rising memory costs alter the economics of AI infrastructure itself. I believe they do—but not in the way many investors currently assume.

The Memory Story Is Real

According to SemiAnalysis, combined spending on DRAM, NAND, and HBM inside Nvidia AI systems will exceed 30% of system cost by the end of 2026 and surpass 40% during 2027. The firm also projects memory’s share of hyperscaler AI infrastructure spending to rise sharply as HBM shortages persist, DRAM prices remain elevated, and memory manufacturers continue allocating production toward AI products. Their conclusion reinforces what memory manufacturers have already begun reporting through higher average selling prices and record profitability.

The evidence supporting this trend extends beyond current pricing. Each generation of Nvidia accelerators requires dramatically more memory capacity and bandwidth than its predecessor. HBM stacks continue growing in capacity, interface width, and manufacturing complexity, while qualification cycles lengthen and supply remains constrained. These developments are structural rather than cyclical. Memory is becoming increasingly valuable because AI architectures require exponentially greater movement of data as well as greater computational capability.

Yet the significance of SemiAnalysis’ findings extends beyond the composition of an AI server bill of materials. Much of the current discussion has focused on the percentage of system cost represented by memory, but that metric alone says little about investment performance. A rack containing 40% memory can produce outstanding returns if it generates sufficiently high inference revenue over its operating life, while a rack containing only 20% memory can prove uneconomic if utilization, pricing, or workload demand falls short of expectations. For investors, the more meaningful question is not how much memory resides inside an AI system, but whether the revenue generated over that system’s useful life justifies the capital required to build and operate it. Viewed from that perspective, memory inflation becomes one variable within a much broader framework of AI infrastructure economics rather than the investment thesis itself.

According to Table 1, the growth in memory spending is substantial regardless of whether one measures it as a percentage of Nvidia system cost or broader hyperscale AI infrastructure investment. SemiAnalysis projects memory’s share of Nvidia systems to rise from approximately 10%–15% only two years ago to more than 30% by the end of 2026 and above 40% during 2027. Their broader analysis similarly concludes that memory’s share of hyperscaler AI capital expenditures is increasing rapidly as HBM supply remains constrained and conventional DRAM prices continue rising. These projections underscore an important reality: memory has become one of the principal economic drivers of AI infrastructure rather than simply another component within it.

The conclusion itself is difficult to dispute. Where I believe investors should extend the analysis is in understanding what these numbers actually imply. A larger memory bill does not automatically produce a weaker investment, just as a smaller memory bill does not guarantee a superior one. Capital-intensive industries have always been evaluated according to the returns generated by those investments rather than the composition of the capital itself. Airlines are not valued according to the percentage of an aircraft represented by engines, nor are electric utilities valued according to the percentage of a generating station represented by turbines. Investors evaluate whether those assets generate acceptable cash flow over their useful lives.